The Murrin Decision: How Long Should You Keep Tax Records?

If you’ve ever asked, “How long do I actually need to keep my tax records?”—you’re not alone.

A recent court case, Murrin v. Commissioner, is a great reminder that the answer isn’t always as simple as “three years.”

Let’s break it down in plain English.

What Was the Murrin Decision About?

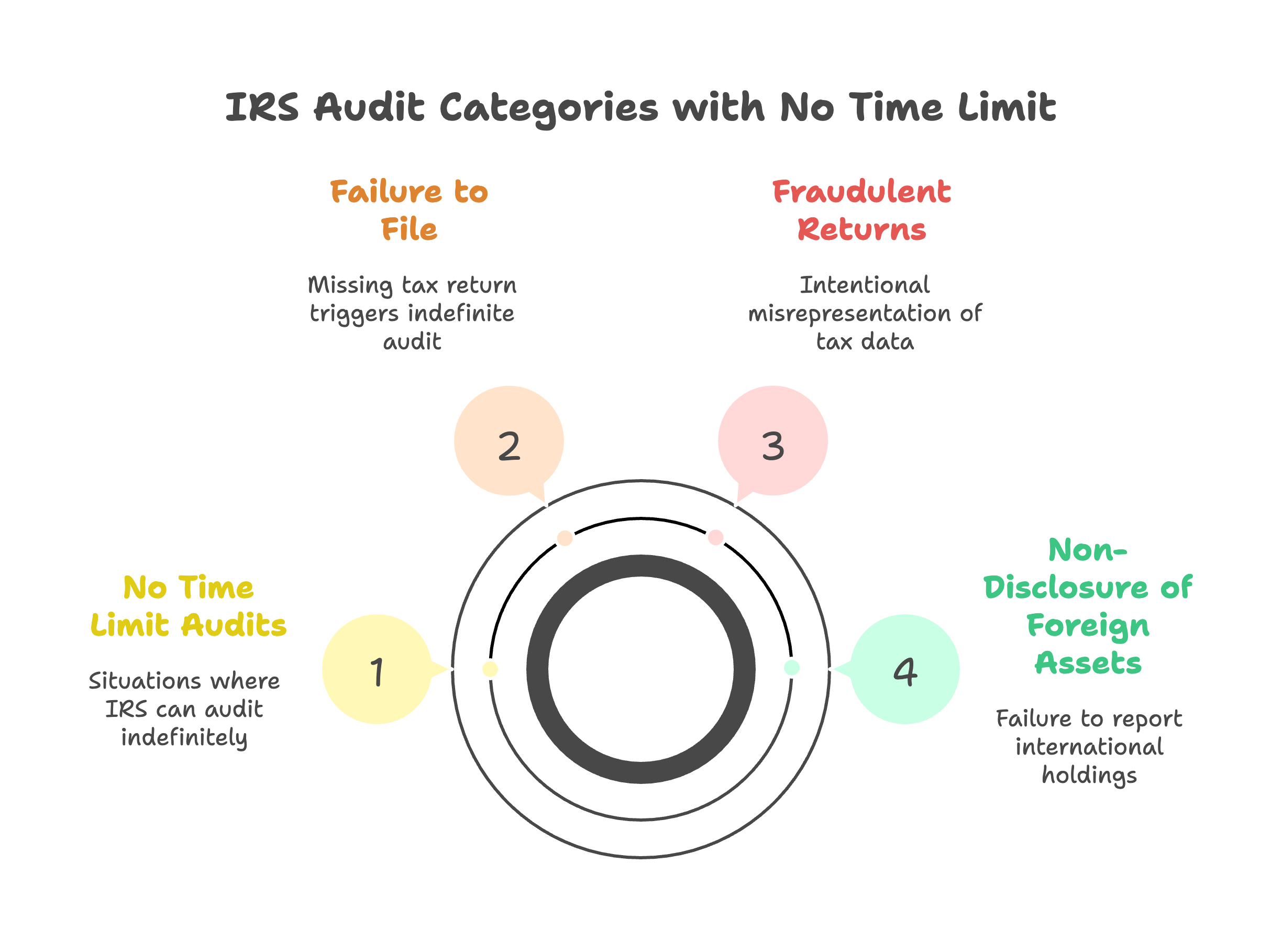

In the Murrin case, the taxpayer was audited and asked to support deductions from prior years—but didn’t have the records anymore. The IRS's unlimited audit window under Section 6501(c)(1) applies even when the taxpayer had absolutely no intent to evade taxes.

The result?

👉 The IRS disallowed the deductions.

👉 The taxpayer lost the case.

The key takeaway:

If you can’t prove it, you can’t deduct it—even if it was legitimate.

The “3-Year Rule” (and Why It’s Misleading)

You’ve probably heard:

“Keep tax records for 3 years.”

That comes from the general IRS statute of limitations—the time the IRS has to audit a return.

But here’s where it gets tricky:

The IRS can go back longer if:

You underreport income by more than 25% → 6 years

There’s fraud or no return filed → no limit

You claim certain losses or credits → longer review periods

You carry items forward (like depreciation or NOLs)

So in reality…

👉 3 years is the minimum—not the safe rule.

What You Should Keep (and For How Long)

Here’s a practical breakdown for your clients:

1. Tax Returns

Keep forever

They’re your financial “history file”

2. Supporting Documents (Receipts, Expenses, Bank Statements)

Minimum: 3 years

Safer: 6–7 years

This includes:

Expense receipts

Bank & credit card statements

1099s, W-2s, etc.

3. Assets & Depreciation Records

This is where most people mess up.

👉 Keep for the life of the asset + 3–7 years after disposal

Examples:

Equipment purchases

Vehicles

Real estate

Why?

Because the IRS can audit the gain/loss calculation years later, and that depends on your original records.

4. Business Ownership & Entity Documents

Keep forever

Includes:

Formation docs

Ownership records

Equity contributions

Real-World Example (Why This Matters)

Let’s say a client:

Bought equipment in 2018

Fully depreciated it

Sold it in 2025

If they tossed the 2018 records?

👉 They may not be able to prove basis

👉 That could mean paying tax on more gain than necessary

This is exactly the type of situation cases like Murrin highlight.

The Practical Rule I Recommend

👉 Keep everything for 7 years minimum

👉 Keep asset-related records much longer

👉 Store it digitally so it’s not a burden

Storage is cheap. Recreating records during an audit is not.

A Better Way to Store Receipts (Without the Paper Pile)

Keeping records doesn’t mean keeping stacks of paper.

The easiest (and most reliable) way to stay organized is to store everything digitally—and attach documentation directly to the transaction.

Here’s how that works in practice:

👉 Upload receipts to a secure client portal

👉 Each receipt is reviewed and matched to the correct transaction

👉 The document is attached directly inside QuickBooks Online

So instead of digging through folders later…

Everything is already where it should be.

Why This Matters

If the IRS ever asks questions:

You don’t have to search your email

You don’t have to dig through paper files

You don’t have to guess what a charge was

👉 It’s all tied directly to the transaction in your books

What I Recommend to Clients

Keep it simple:

Upload receipts as you get them (or once per week)

Use a single system—not random folders

Let your bookkeeping system do the organizing for you

This turns recordkeeping from something you “catch up on”…

into something that’s handled automatically throughout the year.

The Real Benefit

This isn’t just about audits.

It’s about:

Cleaner books

Faster month-end close

Fewer questions and back-and-forth

And no scrambling at tax time

Final Takeaway

The Murrin decision reinforces a simple truth:

Good bookkeeping isn’t just about reports—it’s about documentation.

If records are missing, even valid deductions can disappear.

Want Help Staying Organized?

If your books (or your document storage) are a mess, that’s exactly what we fix.

Clean books. Clear records. No scrambling if the IRS ever asks questions.

The 5 Signs Your Books Need a Clean-Up (Before Tax Season Gets Ugly)

Messy books usually start small — until tax season arrives.

Most business owners don’t realize their bookkeeping needs attention until something forces the issue.

Usually it’s:

Tax season stress

A CPA asking uncomfortable questions

Cash flow that doesn’t make sense

Or reports that simply don’t look right

The reality is that bookkeeping problems build slowly over time — and the longer they sit, the harder (and more expensive) they become to fix.

Here are five warning signs I commonly see when reviewing books for Phoenix small businesses.

🚩 1. Your Bank Accounts Aren’t Reconciled

This is the biggest red flag.

If accounts aren’t reconciled monthly, your financial reports quickly become unreliable.

Common symptoms include:

Ending balances that don’t match statements

Duplicate transactions

Missing expenses or deposits

Numbers changing unexpectedly month to month

Reconciliation isn’t optional bookkeeping maintenance — it’s the foundation everything else sits on.

🚩 2. Uncategorized Transactions Keep Piling Up

If your bookkeeping shows dozens (or hundreds) of transactions categorized as:

Uncategorized Expense

Ask My Accountant

Suspense or clearing accounts

…it usually means bookkeeping has fallen behind.

These transactions create inaccurate reports and often lead to missed deductions or incorrect financial decisions.

Small problems compound quickly here.

🚩 3. Your Profit Looks Good — But Cash Feels Tight

This is one of the most common frustrations business owners experience.

Your Profit & Loss statement shows profit, yet:

The bank balance feels low

Credit cards keep growing

Taxes come as a surprise

This disconnect typically means timing issues, misclassifications, or incomplete bookkeeping.

Your reports may technically run — but they’re not telling the real story.

🚩 4. Negative Balances Appear in Strange Places

Certain accounts should almost never be negative.

Examples I frequently see during clean-ups:

Negative Undeposited Funds

Negative Accounts Receivable

Vendor balances that don’t make sense

Old transactions lingering for years

These usually signal workflow issues rather than simple mistakes — and they rarely fix themselves.

🚩 5. Your Accountant Requests Adjustments Every Year

If your CPA regularly says things like:

“We had to make several adjustments.”

“Your books needed cleanup.”

“Next year let’s try to keep things cleaner.”

That’s a strong indicator your bookkeeping system needs improvement.

Clean books reduce tax prep costs, stress, and surprises.

✅ The Good News

Most bookkeeping issues are completely fixable.

In many cases, a structured clean-up project can:

Restore accurate financial reports

Prepare books for tax filing

Improve cash visibility

Create a solid foundation going forward

The earlier problems are addressed, the easier the solution becomes.

💡 When to Consider a Bookkeeping Clean-Up

If you recognize two or more of these signs, it’s usually time for a professional review.

A clean-up isn’t about assigning blame — it’s about getting clarity so your numbers actually support business decisions.

📍 How I Help Phoenix Business Owners

At Go Get Geek!, I help small businesses:

Clean up and organize QuickBooks Online

Reconcile accounts properly

Produce tax-ready financial statements

Transition into reliable monthly bookkeeping

Because accurate books shouldn’t only exist once a year at tax time.

📞 CALL TO ACTION

Why Your Profit & Loss Statement Isn’t Telling You the Truth

If your Profit & Loss statement looks healthy… but your bank account doesn’t — you’re not alone.

I see this all the time working with small business owners in Phoenix. They run a Profit & Loss report in QuickBooks Online, see a profit, and assume everything is fine.

Then reality hits:

Cash feels tight

Taxes are higher than expected

Or they’re asking, “Where did the money go?”

Here’s the truth:

Your Profit & Loss report isn’t lying — but it also doesn’t tell the full story.

1️⃣ Profit Does NOT Equal Cash

This is the biggest misunderstanding I see.

Your Profit & Loss shows accounting profit — not available cash.

A few common examples:

You send invoices → income shows immediately (even if unpaid)

You buy equipment → cash leaves the bank, but expense may be spread out

Credit card expenses hit reports before cash actually leaves

So yes… your business can show a profit while feeling broke.

That doesn’t mean you’re doing anything wrong — it just means the numbers need context.

2️⃣ Cash vs Accrual Can Change Everything

Another common issue is timing.

Depending on how your books are set up, reports may show:

Income when it’s earned (accrual)

OR when money moves (cash basis)

That means:

December sales paid in January could make one month look amazing — and the next look terrible.

Same business. Same transactions. Completely different story.

This is why understanding your report settings matters.

3️⃣ Misclassified Transactions Quietly Wreck Your P&L

This is where bookkeeping quality really shows.

A Profit & Loss report is only as clean as the data underneath it.

Common issues I fix during clean-up projects:

Owner draws coded as expenses

Personal purchases mixed into business

Loan payments showing as expenses

Uncategorized transactions sitting for months

One or two errors won’t kill your reports.

Hundreds will.

4️⃣ Payroll Costs Are Bigger Than Most Owners Realize

Many owners look at net pay and think:

“That’s my payroll cost.”

But payroll includes:

Employer taxes

Benefits

Payroll processing fees

Timing differences between pay periods

This often explains why profit swings wildly month to month — even when revenue is stable.

5️⃣ Your Profit & Loss Is Only One Piece of the Puzzle

A good bookkeeper doesn’t just look at one report.

We’re also looking at:

Balance Sheet

Cash flow trends

Aging reports

Debt vs equity

Think of your Profit & Loss like one chapter of a book — not the whole story.

What This Means for Small Business Owners

If your numbers feel confusing, you’re not bad at business.

Usually it just means:

➡️ The bookkeeping underneath needs attention.

Once the books are clean, your reports start making sense — and decisions get easier.

💡 How I Help

I work with Phoenix small businesses to:

Clean up messy books

Make QuickBooks reports actually useful

Provide clear, tax-ready financial statements

Because a good Profit & Loss should answer questions — not create more of them.